If you run or work with a charity, you probably already know how tricky VAT can be. The rules are not always clear, and most people just assume charities are “exempt” from VAT altogether. The truth is not that simple.

Charities in the UK do not get a free pass on VAT. They pay it on most goods and services just like any business or individual. But in some situations, they can reclaim VAT or avoid paying it in the first place. And knowing the difference can save a charity thousands of pounds each year.

So let us break it down.

What Exactly Is A Charitable Organisation?

As per HMRC not every organisation that does good work automatically qualifies as a charity. An organisation is considered a charity if it meets the following conditions:

- It is Established solely for charitable purposes

- It is subject to the control of the High Court in England and Wales, the Court of Session in Scotland or the High Court in Northern Ireland in the exercise of its jurisdiction over charities.

- It is registered with the Charity Commission (in England and Wales) or the relevant regulator in Scotland or Northern Ireland unless exempt or excepted from registration.

Only charities recognised under UK law can claim VAT reliefs. Other not-for-profit groups, social enterprises or community organisations may do valuable work but will not necessarily qualify for VAT exemption.

VAT Exemptions for Charities

Generally, VAT rules apply to charities the same as any other organisation. Just like a non-charitable business, a charity must register for VAT. The condition is that it generates taxable sales that exceed the VAT threshold (£85,000).

Once registered, they can charge VAT on goods and services they provide. Moreover, they have the responsibility to submit VAT returns after three months.

Charities also need to pay VAT on the standard-rated goods and services they buy from businesses that are VAT-registered. However, there are some VAT reliefs and exemptions that are specifically available for charities.

Hence, they’re allowed to pay VAT at a reduced rate of 5 per cent or zero rates when they make purchases.

VAT Relief for Charities

Normally, non-charity organisations don’t get VAT relief and need to pay the full 20% of the VAT to their supplier. But a charity organisation – even if it is not registered – can request its suppliers to charge the reduced rate of 5% or zero rate (0%) of VAT for some goods and services.

Moreover, charity organisations also don’t need to pay VAT for qualifying goods that are imported from outside the EU.

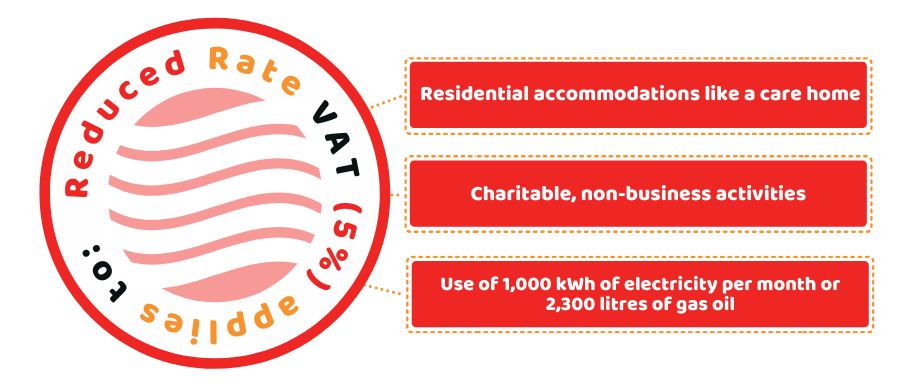

Goods and Services Taxed at Reduced Rate (5%)

VAT on qualifying fuel and gas is charged to charities at a reduced rate of 5%. But to qualify for the discounted rate of VAT, the resources need to be used for:

- Residential accommodation, like a care home or children’s home

- Charitable, non-business activities like providing free childcare

- Use on a small scale up to a maximum of 1,000 kWh of electricity per month or 2,300 litres of gas oil

Note: You need to keep in mind that qualifying fuel and power don’t include vehicle fuel.

If you are using the energy supply for both business and charitable purposes, you need to pay the standard rate on the portion of your bill that is used for business purposes.

If less than 60% of the energy you consume qualifies for reduced-rate activities, you have to pay the standard rate of 20% VAT for the rest. However, if you’re using over 60% fuel and power on reduced-rate activities, the reduced rate is chargeable on your whole bill.

Goods and Services Taxed at Zero Rate (o%)

Charity businesses may also qualify for purchasing a wide range of goods and services at zero VAT, including:

- Medical supplies and equipment

- Aid for disabled people

- Construction and building work

- Scientific equipment

- Advertising

- Rescue equipment

- Vehicles, such as ambulances and lifeboats

You can get the list of qualifying goods and services at a zero rate on the HMRC website.

Imported Goods

Charity organisations are exempt from VAT on goods that are imported from outside the UK, provided they benefit people in need. HMRC defines those as:

- Necessities

- Equipment and office materials for needy people

- Goods that are going to be used or sold at charity events

Can Charities Claim Back VAT?

If a VAT-registered charity organisation is paying input tax (standard rate VAT) on some goods and services, it may qualify to claim back VAT. However, you need to remember that if your charity organisation is not VAT registered, it won’t be able to reclaim VAT charged on the purchase of goods and services from VAT-registered businesses.

Registered charity organisations can reclaim VAT if:

- They fall within HMRC’s definition of a charity for VAT purposes

- Recognised for tax purposes (recognised by HMRC and registered with the Charity Commission)

- Goods and services they bought qualify for reduced or zero rate

If you meet the above conditions, you can reclaim up to four years of the back pay you made for VAT. The amount that you will recover will be the difference between the standard rate and the zero or discounted rate. You’d be happy to know if you were eligible for discounted or zero-rate VAT and had been paying the standard rate.

You need to bear in mind that if your charity organisation is erroneously paying zero or discounted rates, HMRC may reclaim the amount that is due to you for the past years. And you might be charged with hefty tax charges. So, to be protected you need to make sure that you are eligible for charity VAT relief.

How Charities Can Claim VAT Relief?

To get goods and services at zero-rate VAT or a reduced rate, charity organisations should provide evidence of their charitable status. You can either provide a recognition letter from Charity Commission Registration or HMRC if your organisation is located in England or Wales.

Can Charities Reclaim VAT on Fundraising Events?

This is a common question. Fundraising events often fall into a special category.

- If the event is purely to raise money for the charity and meets HMRC’s conditions, the income may be exempt from VAT.

- But that also means the charity cannot reclaim VAT on the costs linked to the event.

So while the event itself might not attract VAT, the trade-off is that the input VAT may not be recoverable.

Can Charities Claim Back VAT on Building Work?

Yes, but only in some cases.

Charities can get zero-rating or relief on building projects if:

- The building is used for charitable purposes only, such as providing free welfare or education services.

- It is not used for business or commercial activities.

If the building is used for both the charitable and business purposes then the VAT situation becomes more complicated and usually requires professional advice.

How Do Charities Actually Claim Back VAT?

The process is similar to businesses. If the charity is VAT registered:

- It files VAT returns with HMRC.

- Input VAT (VAT paid on purchases) is deducted from output VAT (VAT charged on sales).

- If more VAT is paid than collected, the charity can reclaim the difference.

For zero-rated or VAT-exempt purchases, charities usually have to provide suppliers with a certificate confirming their charitable status and the reason for VAT relief.

What Is the Difference Between VAT Exempt and Zero-Rated for Charities?

This is one of the biggest areas of confusion.

- Zero-rated means VAT is charged at 0 percent. Charities still record the transaction as taxable which means they can often reclaim VAT on related costs.

- Exempt means no VAT is charged but the transaction is outside the VAT system. That usually means input VAT cannot be reclaimed.

What Are the Most Common Situations Where Charities Can Claim Back VAT?

- Advertising campaigns for fundraising or awareness.

- Equipment and services for disabled people.

- Construction of a new charitable building used for non-business activities.

- Fuel and power used for residential or charitable non-business purposes.

What About Grants and Donations – Do They Affect VAT?

Grants and donations are generally outside the scope of VAT. That means they are not treated as payment for goods or services.

So while they do not generate VAT, they also do not allow the charity to claim back VAT on related costs, since there is no taxable business activity linked to them.

Quick Sum Up

To sum up the discussion, we hope that you have got the answer to can charity claim back VAT. Charity organisations that are VAT registered can reclaim the VAT on purchases of goods and services.

Unlike non-charity businesses, charities enjoy the discounted and zero rate VAT on many goods and services, along with some items that are imported to the UK.

Disclaimer: This blog is written for general information on reclaiming VAT for charities.