Limited cost traders are ‘work just’ organizations that need to utilize the 16.5% rate when utilizing the Flat Rate VAT scheme. Limited cost trader alluded to as limited cost business, is a sort of business class that was acquainted by HMRC with try not to possibly affect the Flat Rate VAT Scheme.

Who is viewed as a Limited cost Trader?

The 16.5% flat rate will apply to any business that is viewed as a limited cost trader. Your business falls into this classification in the event that one of the accompanyings applies:

- The VAT comprehensive cost of buying products is under 2% of your yearly turnover.

- The VAT comprehensive cost of buying products is over 2% of your yearly turnover, yet less than £1000 each year.

The products remembered for these computations have a few limitations which will be laid out in the following area.

Planning to retire in the next few years? Plan ahead, let’s talk!

Limited Cost Trader – Significant Products:

On the off chance that you fall inside the classification of a limited cost trader, you should initially compute your yearly VAT comprehensive measure of products bought. This incorporates any products utilized rigorously for business purposes, aside from the accompanying:

- Capital costs – any products purchased to be utilized throughout an extensive stretch of time, like a PC.

- Food and refreshments bought for the business or representatives.

- Anything identified with vehicles (fuel, vehicle acquisition, parts, and so forth) except if your business is a vehicle administration, for example, a taxi organization.

If you include the entirety of the products bought in the year, barring the ones referenced above, and it adds up to under 2% of your turnover or under £1000, then, at that point, you are a limited cost trader. Invoicing programming can assist you with dealing with all parts of your business accounts.

Your bookkeeping reports will naturally mirror the right information at a flat rate. You can present your VAT Report straightforwardly to HMRC in only a couple of snaps. Whenever you make a receipt, enter a cost, or add an instalment, the reports, for example, your monetary record will mirror the new data continuously.

What is the Flat Rate VAT scheme?

To lessen the weight of this record-keeping on more modest firms, HMRC offers a Flat Rate Scheme. With this scheme, as opposed to paying HMRC what you’ve gathered in VAT on your business short the VAT you’ve asserted for on costs, you basically need to pay HMRC a set level of your deals. This implies little firms by and large don’t have to follow VAT on buys.

Can’t find what you are looking for? why not speak to one of our experts and see how we can help you are looking for.

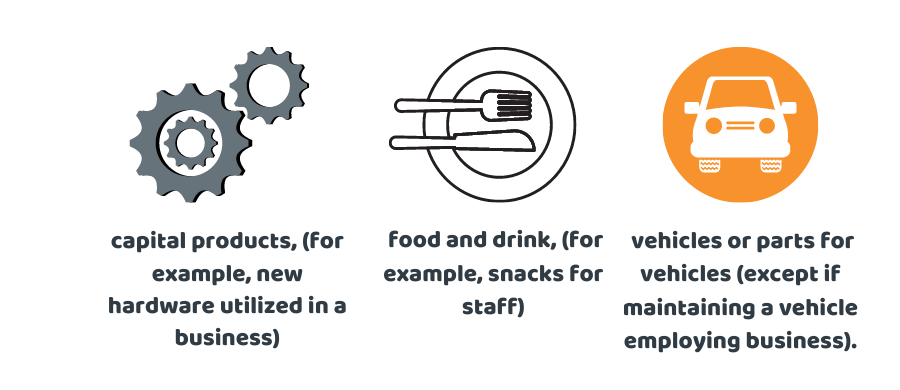

When working out the sum you have spent on products, you can exclude the acquisition of:

- capital products, (for example, new hardware utilized in a business)

- food and drink, (for example, snacks for staff)

- vehicles or parts for vehicles (except if maintaining a vehicle employing business).

In the event that a firm spends under £1,000 in their bookkeeping period (if the period was a year), they consider ‘work just’ regardless of whether this is over 2% of your deals. In the event that your bookkeeping period is longer/more limited than a year, the £1,000 edge is favourable to rate in like manner.

Conclusion:

To sum up the discussion we can say that, the developing number of independently employed have been referred to as a reason for declining charge incomes. In any case, our experience and exploration show that individuals run their own organizations for business reasons, not to stay away from charge.

Still, have a question? Get in touch with us.

Disclaimer: This content includes general information on the limited-cost traders.