If you are an individual who is in more than one job, you absolutely need to know everything about the tax on a second job. In order to avoid paying too much tax or too little that might cause you trouble later on. Paying too much tax is neither good for you nor for your pocket.

The important to know first is that if it is a viable option to go for a second job. Start checking your current job description to figure out if it stops you to go for a second job or not. To avoid any kind of conflicts, like:

- Is there any clause that prevents you to take more work?

- Speak to your current employer about it to be clear.

- Once you are clear about it, you are good to go for a second job.

Speak to our Experts for professional advice about tax on second jobs!

Tax On Second Job – The Basics:

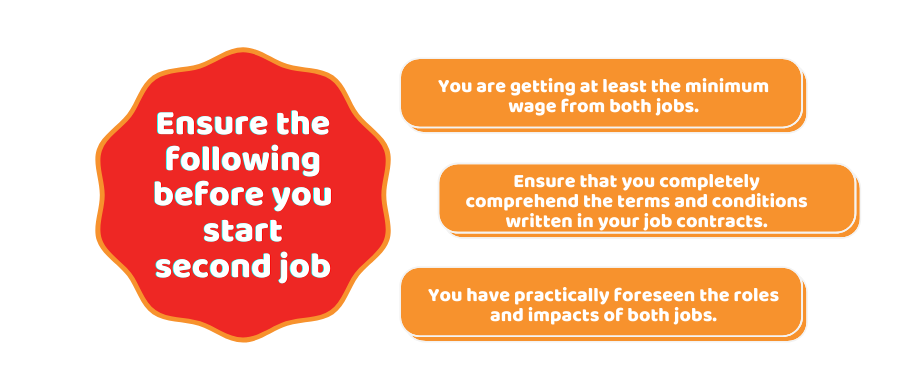

Once you are self-assured about the rules regarding second job prevention, you need these important points to keep under serious consideration.

- You are getting at least the minimum wage from both jobs.

- Ensure that you completely comprehend the terms and conditions written in your job contracts.

- You have practically foreseen the roles and impacts of both jobs.

HMRC And Tax System:

According to the tax system, one job is your main income. You get your personal allowance of 11,850 pounds from this. This is the amount that you get before you consider paying the tax.

The income you get from a second job is the cherry on top. Also, with this income, you will not get any personal allowance. The chances are that you pay more tax on this second income source. There is a smart choice of adding this amount to your main income and you will have to pay the same amount of tax on a second job overall.

Meet your business needs beyond just numbers and figures with Accotax, contact us now!

How Much Tax Shall I Pay – Second Job:

The extent of your tax payment totally depends on the amount you are paid as salary from both the jobs. In case your first job is below the personal allowance, generally, the tax on a second job will be a standard 20%. Let’s take a practical example of an employee who gets 150npounds each week from his first job. Whereas, he withdraws 100 pounds every week from his second job.

Since the first job is below the personal allowance, so, no tax will be charged on the first job. However, the second job will be considered for charging tax at 20%. Often tax on a second job is paid via the BR tax code. The question that arises here is what is the BR Tax code?

BR is the abbreviation of Basic Rate. the standard basic rate is 20%. There is the possibility that extra income can lead to paying more tax for a year in case the earnings exceed the amount of 46,351 pounds. The situation in which you might be paying too little or too high tax is given below.

Paying Little Tax: In case you have not informed HMRC and getting another personal allowance on the second job.

Paying Little Tax: You pay basic tax on both jobs while your second job makes you a high rate tax band.

Paying Too Much Tax: This happens when the salary you take from both jobs is less than your personal allowance.

Avoid Under And Over-paying Tax:

It is important to get a starter form P46 from your employer when you start a new job. This form includes the details of other jobs and it is then sent to HMRC. It is also suggested to ensure your tax codes. Generally, the second job has the BR code after a number.

Pensions and Second Job:

Ensure the hold of records and details if there is a possibility of pension in your second job. In case you are making less from your second job and this makes you pay less into the pension as well. It is suggested to put this amount with other pension pots when you decide to leave the second job.

Know more about how much national insurance you will pay if you are into two or more jobs with our professionals at Accotax!

Conclusion:

To conclude the discussion we can say that there is no way to escape from Tax on a second Job. The suggestion is to inform HMRC about it and make the smartest way out to pay tax on a second job with the above recommendations. We hope this blog is convincing enough to make you follow the guided rules.

For further information and taxation services, get in touch with our Accountants now!