In case you utilize full-time, low maintenance, or getting a private annuity you will have gotten a letter from HMRC with a refreshed tax coding recently (as a rule around Feb/March). HMRC needs to give this on the grounds that they have all the data on your own pay and any allowances they need to take from you. In this blog post, we’ll talk about what is Tax Code 1257L? And how one check their tax code whether it’s correct or not.

Tax Codes:

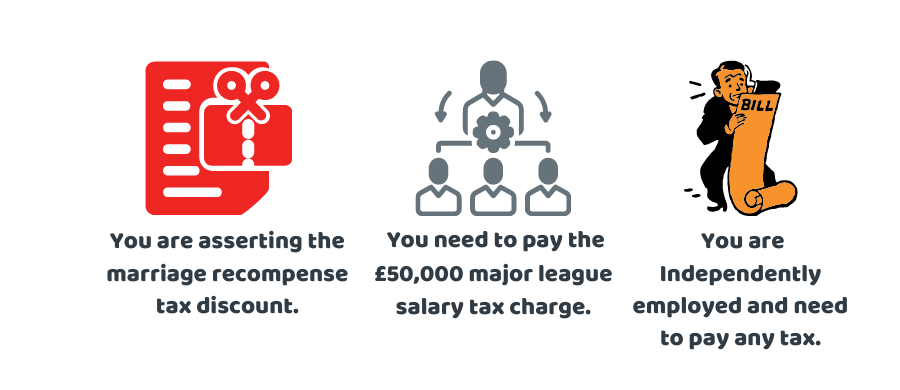

Your tax code goes on for one tax year so both you and your boss will probably get a coding notice before the beginning of another tax year. You may get a letter from HMRC to change your tax code if your conditions change, for instance, if:

- you are asserting the marriage recompense tax discount.

- need to pay the £50,000 major league salary tax charge.

- are independently employed and need to pay any tax you owe through your PAYE tax code.

How would I Know my Tax Code?

Your organization needs to give you a payslip, so in case you don’t know how to get to it, ask your boss for direction. You can likewise utilize the public authority’s online tax checker device to see your tax code.

Still, have a question? Get in touch with us.

What Is Tax Code 1257L?

Almost everybody in the UK is qualified for a sans tax individual stipend, which implies that a specific measure of your profit every year is paid to you without being taxed.

HMRC changed over the individual stipend of £12,570 and transformed it into tax code 1257L. The letter L is added in case you are eligible for the standard individual stipend. This outcome is in tax code 1257L. So in straightforward terms, on the off chance that you have a tax code 1257L, it implies that you can procure £12,570 before you settle tax.

The Tax Amount You will Need To Pay With Tax Code 1257L:

The tax code 1257L is an aggregate code. That implies you’ll get a piece of your own stipend each time you get compensated. For instance, in case you are paid month to month, you’ll get £1,047.50 (£12,570 ÷ 12) sans tax every month you get compensated. That way before the finish of the tax year, you’ll have accepted your own recompense in full.

Income over this is taxed at 20%. This is for income somewhere in the range of £12,571 and £50,270. After this, it increments to 40% for profit somewhere in the range of £50,271 and £150,000. Profit over £150,001 is then taxed at the most elevated rate which is 45%.

On the off chance that you required a couple of long periods of work and had no other occupation during the tax year, you’ll get all the individual recompense you are owed in your first payslip on the off chance that you start a new position.

In case you’re searching for help with getting back tax discounts from the UK HMRC, reach out to our experts now.

What are Emergency Tax Codes 1257 W1, 1257 M1, 1257 X?

This regularly occurs on the off chance that you:

- Start a new position and not given a P45

- Start working for a business after you’ve halted independent work

- Get organization benefits, similar to an organization vehicle

- Get State Pension

Having W1 or M1 joined to your code implies it is a non-combined tax code. The tax due on every instalment is not really set in stone without considering any tax you’ve effectively paid for this present year, or the amount of your sans tax individual stipend has been utilized.

All in all, it can bring about your overpaying tax.

Despite the fact that crisis tax codes are brief while the important data is assembled, it implies you’ll pay tax on the entirety of your pay over the individual recompense and not get any accumulation of individual remittance you might be qualified for yet haven’t utilized.

I have a 1257L Tax code, is My Tax Code Wrong?

Tax code 1257L will be right for most representatives. Regularly, those with only one work and without any advantages or tax-deductible recompenses will have a right tax code. Nonetheless, the tax coding framework can rapidly turn out badly. Average models include:

- A difference in positions, having more than 1 work, beginning, leaving, or resigning in the year.

- Having more than 1 type of revenue like a task and an annuity.

- Changes to taxable advantages e.g being furnished with an organization van for private use.

How Do I Correct My Tax Code?

When you understand there has been a misstep with your PAYE tax code you should reach out to HMRC by email or telephone (0300 200 3300). You ought to give all the important, precise data so they can work out your right tax code.

Assemble these before you contact HMRC:

Complete name (counting center names)

Date of birth

- Email address

- Public Insurance Number

- Manager/benefits supplier tax reference number

- The worker works number or benefits number (private as well as organization)

- Organization benefits (for example medical services, vehicle fuel recompense)

- Some other pay (for example investment funds revenue, property rental)

- A week after week State Benefits or State Pension instalments

Why is it Essential to get your Tax Code Revised?

On the off chance that there is a mistake with your tax code, you are paying some unacceptable measure of tax. On the off chance that you have paid excessively, you can recover the excessive charge, as long as you are inside HMRC’s cutoff times. Assuming you have paid nearly nothing, you need to reimburse HMRC. In any case, it is smarter to discover sooner than later.

Conclusion:

To conclude, we can say that if you end the tax year on a crisis tax code, HMRC will include how much tax you have paid and worked out whether you owe anything toward the finish of the tax year. We hope this article helped to develop a better understanding of tax code 1257L.

We offer a top expert adviser help with no secret expenses at Accotax.

Disclaimer: This content includes general information on Tax Code 1257L.